This drastic regulatory rollback marks a massive California rideshare insurance shift. It quietly transfers the financial burden of auto accidents away from multi-billion-dollar tech corporations and dumps it directly onto the personal health insurance policies and bank accounts of everyday Californians. If you use rideshare apps as a passenger or drive for them to earn a living, understanding this legal landscape is no longer optional—it is vital to your financial survival.

The 94% Insurance Cliff: What SB 371 Changed

To grasp the magnitude of this shift, one must look at how rideshare insurance operates. Rideshare liability is divided into distinct “periods” based on the driver’s activity. Period 1 is when the app is open and the driver is logging in, waiting for a match. Period 2 is when a match is accepted and the driver is en route to pick up the rider. Period 3 is the live ride, from the moment the passenger steps into the vehicle until they exit.

To grasp the magnitude of this shift, one must look at how rideshare insurance operates. Rideshare liability is divided into distinct “periods” based on the driver’s activity. Period 1 is when the app is open and the driver is logging in, waiting for a match. Period 2 is when a match is accepted and the driver is en route to pick up the rider. Period 3 is the live ride, from the moment the passenger steps into the vehicle until they exit.

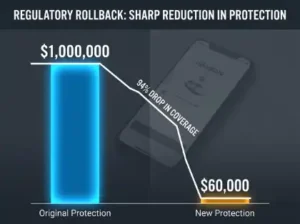

Historically, California required rideshare companies to maintain $1 million in total liability and UM/UIM coverage throughout Periods 2 and 3. This meant that if a reckless, uninsured driver ran a red light and smashed into your rideshare vehicle, causing severe injuries, the rideshare company’s policy would step in to cover your medical bills, lost wages, and pain and suffering up to seven figures.

Under the revised framework of SB 371, while the third-party liability limits (when the rideshare driver causes the crash) remain high, the protections against uninsured or hit-and-run drivers during Period 2 and Period 3 were quietly decimated. The new statutory minimums are a mere fraction of what they used to be. If an uninsured driver hits your Uber or Lyft today, the maximum corporate coverage available to treat your injuries is capped at just $60,000. In an era where a single night in a California emergency room can easily exceed that amount, passengers are rapidly discovering that they are dangerously underinsured.

The Domino Effect on Your Personal Health Insurance

When corporate commercial auto policies scale back so aggressively, the medical bills do not simply vanish. Instead, the cost of treatment triggers a complex and stressful domino effect that ends at your front door.

If you suffer a severe injury—such as spinal trauma, broken bones, or a traumatic brain injury—resulting from an accident caused by an uninsured motorist while riding in an Uber, the $60,000 corporate cap will likely be exhausted within the first few hours of your hospitalization. Once that commercial limit is breached, hospital billing departments immediately look for alternative payment sources. This is where your personal health insurance policy is forced to step into the breach.

Relying on personal health insurance for an auto accident introduces a host of systemic headaches for consumers:

- Sky-High Deductibles and Out-of-Pocket Maximums: Unlike commercial auto insurance, which traditionally covers medical costs from dollar one, your health insurance requires you to meet your yearly deductible and clear out-of-pocket maximums, which can cost thousands of dollars.

- Network Restrictions and In-Network Chaos: If the ambulance takes you to an out-of-network trauma center, or if you require specialized long-term physical therapy from a doctor who doesn’t accept your specific health insurance plan, you could be left holding the bill for the balance.

- Health Insurance Liens (Subrogation): If your health insurance provider pays $100,000 for your accident care, and you later recover a small settlement from the rideshare platform’s remaining coverage, your health insurance company has the legal right to place a lien on that settlement to reimburse themselves, leaving you with little to nothing.

The Driver Liability Trap: An Unseen Risk for Gig Workers

Passengers are not the only ones vulnerable to this legislative shift. Thousands of California rideshare drivers are operating under a false sense of security, assuming that the corporate giant they contract with completely covers them while a passenger is in the backseat.

If a rideshare driver is struck by an uninsured motorist and suffers debilitating injuries that prevent them from working, they can no longer look to a $1 million corporate policy to bridge the financial gap. With the limit reduced to $60,000, a driver could easily face career-ending medical bills and long-term lost wages with absolutely no corporate recourse. Furthermore, if a multi-passenger accident occurs and the total medical damages exceed the corporate $300,000 per-accident cap, injured passengers may attempt to sue the rideshare driver individually, putting the driver’s personal assets, savings, and home at serious risk.

How to Protect Yourself: Actionable Steps for Californians

Because the state legislature has rolled back corporate accountability, the responsibility of risk management has shifted entirely to the individual. Fortunately, there are proactive steps you can take right now to build a personal shield against the California rideshare insurance shift.

Because the state legislature has rolled back corporate accountability, the responsibility of risk management has shifted entirely to the individual. Fortunately, there are proactive steps you can take right now to build a personal shield against the California rideshare insurance shift.

1. Review Your Own Auto Insurance Policy for Robust UM/UIM Coverage: If you own a personal vehicle in California, check your policy declarations page immediately. Ensure you carry high levels of Uninsured/Underinsured Motorist (UM/UIM) coverage—ideally $250,000/$500,000 or higher. In many cases, your personal auto insurance policy’s UM/UIM coverage can follow you even when you are riding as a passenger in a commercial rideshare vehicle, effectively filling the massive gap left by SB 371.

2. Consider a Personal Umbrella Policy: For comprehensive protection, look into an inexpensive personal umbrella insurance policy. An umbrella policy provides an extra layer of liability and, in some cases, excess UM/UIM coverage that kicks in when underlying policies (like the slashed rideshare limits) are completely exhausted.

3. Audit Your Health Insurance Policy: Know the limits of your health coverage. If you are a frequent rideshare user, having a health plan with low out-of-pocket maximums and a broad network of preferred hospitals across your metro area can mitigate the financial damage if an accident occurs.

Conclusion: Advocating for a Fairer California

The passage and implementation of SB 371 serves as a stark reminder that what is convenient for massive tech corporations is not always what is good for the citizens of California. Slashed insurance requirements keep platform operating costs low, but they leave millions of riders and drivers exposed to severe financial vulnerabilities. Until consumer advocates and the public can push back and demand a restoration of robust commercial protections, protecting yourself through smart personal insurance planning is your best and only line of defense.